{kind=link}

Crypto exchange platforms in India have seen a spurt in trading volume ever since a Supreme Court order quashed a virtual banking ban on cryptocurrencies

While Indian legislators are in consultation for a regulation which might bring a blanket ban on virtual currencies, Indian tech corporations have stated that banning tech is just not the answer

Indian crypto exchanges are attracting investments from global traders, as they witness a surge in customers amid the pandemic

With India’s Supreme Court lifting the digital banking ban on cryptocurrencies in March this year, global traders seem eager to enter the crypto market in India with investments in local exchange platform. Indian cryptocurrency exchanges have additionally witnessed a spike in buying and selling volume ever because the SC quashed the 2018 Reserve Bank of India (RBI) circular which had introduced a banking ban on cryptocurrency in India, calling it unconstitutional.

Since the SC order, there was a spurt in cryptocurrency-related activities in India, with some crypto exchange platforms reporting a 400% spike in trading activity. According to UsefulTulips.org, the combined monthly trading volume between the Indian Rupee and Bitcoin has almost doubled between March and July on two foreign crypto exchanges, LocalBitcoins of Finland and Paxful of the US. Their total quantity in March was $8.14 Mn. By July the figure had reached $16.26 Mn.

Mumbai-based cryptocurrency exchange aggregator, CoinDCX, had seen a 62% month-on-month (MoM) progress in trading quantity for its product Insta, since the SC order. CoinDCX’s Insta, launched on August 15, 2018, is a fiat-crypto exchange product that lets traders trade in INR.

Users can buy 100+ cryptocurrencies at competitive costs with near zero deposit and withdrawal charges. Also, the corporate stated that coins on Insta are protected through CoinDCX’s best-in-class safety measures. Moreover, different crypto exchange platforms like WazirX, Unocoin, Bitbns, Cashaa, Oropocket amongst others have also witnessed a surge in customers and transactions after the Supreme Court verdict.

According to CoinMarketCap, Mumbai-based crypto exchange platforms, CoinDCX and WazirX, are seeing monthly trading volumes of $8 Mn and $12 Mn respectively. While it stands pale in comparison to the trading volumes for crypto exchange platforms in the West, the signs of what might be an enormous market for crypto trading within the near future are visible.

Global traders are additionally bullish about the same. CoinDCX attracted investments worth $5.5 Mn in two rounds, from a number of global traders together with Bain Capital of the US, in March and May after the favourable court ruling. The world’s largest crypto exchange network, Binance of Malta, acquired WazirX last November, maybe anticipating India’s ban on cryptocurrency trading can be lifted quickly.

While Indian legislators are stated to be conducting inter-ministerial consultations on a draft regulation that proposes a blanket ban on cryptocurrencies in India, the stance of Indian IT and tech firms might be a deterrent. In the speedy aftermath of the SC ruling quashing the banking ban on cryptocurrencies, the National Association of Software and Service Companies (NASSCOM) stated that banning technology was not a solution. India’s largest IT firm firm Tata Consultancy Services (TCS), can be seen to be a firm backer of cryptocurrencies. Last month, the corporate launched a crypto trading platform known as Quartz Smart Solution for banks and investments, in collaboration with blockchain startup Quartz, incubated by TCS.

However, with Indian lawmakers involved about crypto’s links with terror financing, findings additionally backed by the Financial Action Task Force (FATF) — a worldwide watchdog to curb money laundering — it stays to be seen if cryptocurrency will flourish in India, or whether or not the present spurt in progress is nothing but a false dawn.

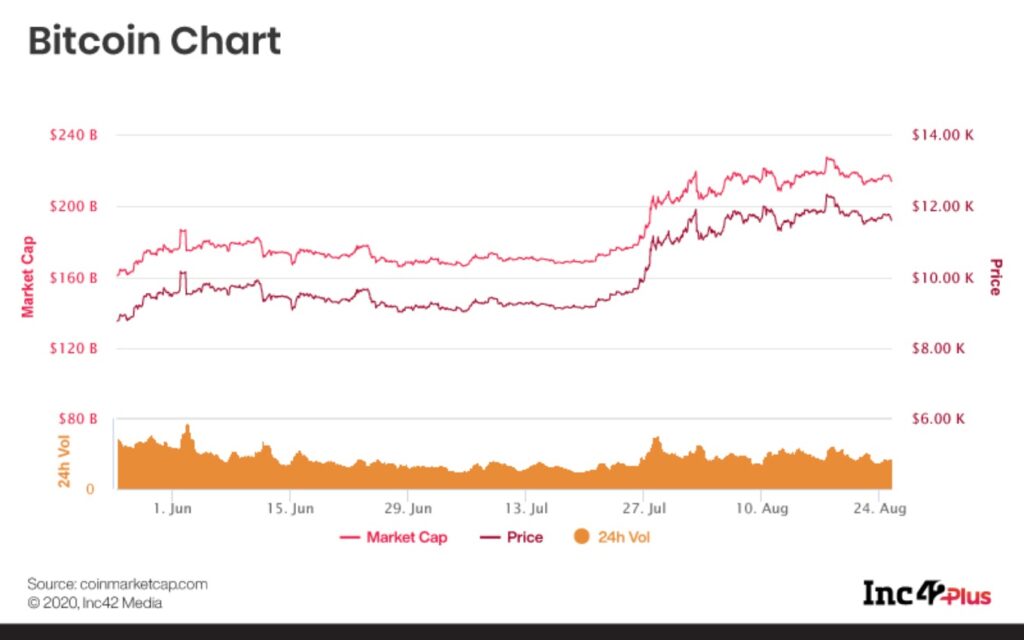

At the time of writing, Bitcoin was trading at $11,767, a decline of 4% from final week, when it was trading at $12,278.

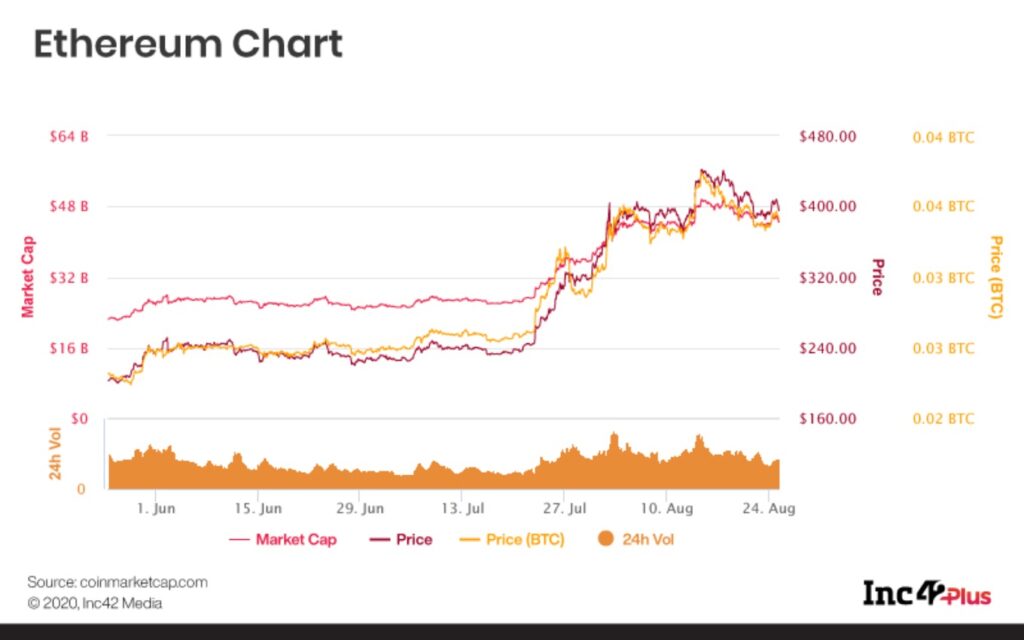

Ethereum was trading at $392.12, a fall of 9% from last week’s $430.95. Its market cap was $43.86 Bn.

The Bitcoin Network Now Consumes 7 Nuclear Plants Worth of Power

The Bitcoin mining process sees miners plugin high-voltage machines, that devour electrical energy as they attempt to solve advanced computational math problems, that are so advanced that they can’t be solved by human hands. The course of is called bitcoin mining, where if the computer is ready to solve the problem, more bitcoin is added to the blockchain network. Hashrate is used to measure the quantity of computing power consumed by the blockchain network.

According to business estimates, the gigawatts of electrical consumption powering industrial bitcoin mining today consumes as much as seven nuclear power plants.

Also Read: Samsung’s Galaxy Book Flex will get 5G and Intel’s 11th Gen Core